IFPI is anticipated to launch the official international recorded music income outcomes for 2024 this month, however within the meantime, the intelligent quantity crunchers at MIDiA Analysis have revealed their very own estimates.

One of many key takeaways from MIDiA’s Recorded Music Market Sharereport, launched on Thursday (March 13), is that this: World recorded music income progress is slowing, and going ahead, artists and rightsholders ought to give attention to rising expanded rights (i.e., higher monetizing superfans) somewhat than relying on streaming income progress.

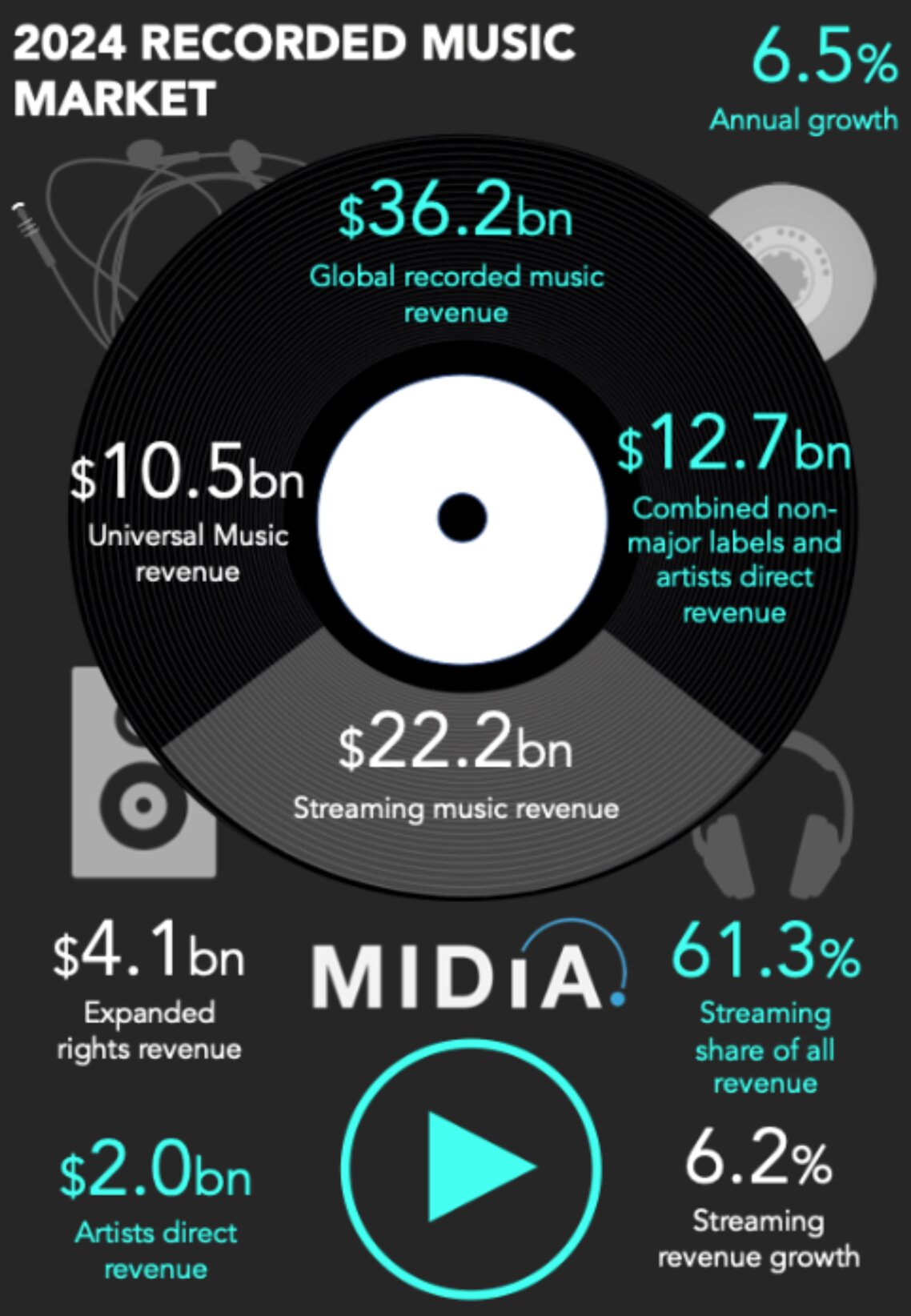

And the headline stat from MIDiA’s new report: World recorded music revenues rose 6.5% YoY to $36.2 billion. That marks a slowdown from 2023, when revenues rose 9.7% YoY, per MIDiA’s estimates.

This 12 months’s MIDiA numbers aren’t instantly similar to prior years, because the analysis agency advised us that “as a result of some modifications to our recognition of non-major label income (together with some removing of double-counted income for labels that additionally act as distributors), complete historic income figures and market shares have modified barely in comparison with earlier editions of this report” and that “as a consequence, all main label market shares have elevated barely.”

The affect of music streaming is “lessening,” MIDiA stated, and 2024 marked the primary 12 months during which streaming’s share of complete recorded music didn’t improve.

In accordance with MIDiA, Streaming income grew 6.2% YoY to $22.2 billion, in comparison with a progress price of 10.3% in 2023. Streaming represented 61.3% of all revenues, versus 62.5% the 12 months earlier than.

“The contribution of streaming to general business progress additionally fell to 58.5%, down from 64.6% in 2023,” MIDiA stated.

“The much-anticipated streaming income deceleration – regardless of current worth will increase – has now arrived. Business consideration is popping to super-premium tiers and new monetization fashions to re-ignite progress.”

MIDiA

The report added: “The much-anticipated streaming income deceleration – regardless of current worth will increase – has now arrived. Business consideration is popping to super-premium tiers and new monetization fashions to re-ignite progress.”

MIDiA suggests future income progress will more and more depend on expanded rights – which means issues akin to merchandise, sponsorships, branding, and different sources of income exterior of gross sales of music itself.

MIDiA’s newest information backs up that assertion. Expanded rights accounted for $4.1 billion in income in 2024, up 17% YoY from $3.5 billion in 2023. That’s a considerably sooner tempo of progress than the remainder of recorded music. Expanded rights accounted for 11.3% of recorded music revenues in 2024, versus 10% in 2023.

(MIDiA counts expanded rights as a part of recorded music revenues. Excluding expanded rights, recorded music revenues in 2024 would have are available in at $32.1 billion.)

Graphic: MIDiA

“With a lot uncertainty within the international financial system, 6.5% annual income progress is an achievement in itself. Nonetheless, the streaming slowdown, coupled with one other down 12 months for bodily, has emphasised a steadily growing quantity of market volatility,” stated Mark Mulligan, Managing Director and Senior Music Analyst at MIDiA Analysis.

“Which makes the quick rising expanded rights phase so necessary for the business. Not solely does it do the essential job of monetizing fandom, it’s quick turning into a hedge in opposition to stodgy streaming progress and the yo-yoing bodily sector.”

When it comes to market share, non-major labels noticed their share of revenues develop for the third consecutive 12 months. Their revenues grew by 8.4% YoY to $5.4 billion, outpacing the 5.4% progress posted by main labels, based on MIDiA.

Among the many majors, solely Sony Music Group (SMG) elevated its market share in 2024. Its 10.2% YoY improve in income resulted in a 700-basis-point improve in market share to 21.7%. Common Music Group, the world’s largest music firm, misplaced 100 foundation factors of market share, MIDiA reported.

“SMG was additionally the quickest rising main label within the first half of the last decade, rising by a complete of 73.9% between 2020 and 2024,” MIDiA famous.

“The quick rising expanded rights phase [is] so necessary for the business. Not solely does it do the essential job of monetizing fandom, it’s quick turning into a hedge in opposition to stodgy streaming progress and the yo-yoing bodily sector.”

Mark Mulligan, MIDiA

Self-releasing artists are additionally on the rise – each when it comes to income captured and within the sheer variety of these artists.

MIDiA’s “Artists Direct” phase – which means self-releasing artists who distribute their music by means of platforms like CD Child, DistroKid, and TuneCore – noticed income improve 4.7% YoY to $2.0 billion in 2024. That’s a barely sooner tempo of progress than the 12 months earlier than, when this phase’s revenues rose 4.5%.

That’s regardless of “headwinds” such because the minimal stream thresholds to obtain payouts from streaming companies, MIDiA famous.

Spotify final 12 months launched a brand new rule that it might now not pay for tracks that obtained fewer than 1,000 performs over the prior 12 months. An identical Deezer’s “artist-centric” cost mannequin has an analogous precept, in that tracks that obtain fewer than 1,000 streams and 500 distinctive listeners per 30 days see decrease royalty payouts than tracks that exceed that threshold.

Nevertheless, DIY artists are dealing with one other “headwind” – the fast improve within the variety of these artists. There at the moment are 8.2 million self-releasing artists, MIDiA stated, and the speed of their progress is three-and-a-half occasions sooner than their revenues are rising.

“One essential aspect to regulate is the lengthy tail of impartial artists,” Mulligan stated.

“Measures like minimal earnings thresholds are taking a toll on Artists Direct income, and serving to main labels throw velocity bumps within the ongoing erosion of their market share. But it’s doing nothing to halt the expansion of releasing artists who compete for ears.”

MIDiA’s international recorded music income progress estimate of 6.5% YoY is roughly in step with Common Music Group’s recorded music income progress within the 12 months to the tip of December 2024: UMG’s recorded music revenues grew 6.4% YoY to €8.901 billion ($9.63bn) in 2024.Music Enterprise Worldwide